Home » Pension 101 » Retirement » Already retired

Pension definitions

| YMPE | Earnings |

|---|---|

| 2020 YMPE | $58,700 |

| 2019 YMPE | $57,400 |

| 2018 YMPE | $55,900 |

| 2017 YMPE | $55,300 |

| +2016 YMPE | $54,900 |

| Subtotal | $282,200 |

| Divide by five | $56,440 |

The annual average of your pensionable earnings for the highest 60 consecutive months of service during the last 120 months of pensionable service before your retirement or termination from the Plan. If you worked less than 60 months, your best average earnings will be based on your average earnings as a member of the Plan.

A temporary benefit provided to employees who retire prior to the age when unreduced CPP benefits begin. It is paid when you retire from your participating employer before age 65 (even if you collect an early CPP pension). The bridge benefit is payable until the earlier of age 65 or your passing.

Learn more about the bridge benefit.

The CPP is a contributory, earnings-related social insurance program that is paid by the federal government. It provides a measure of income to contributors and their families upon retirement, disability, and death. For further details, contact Service Canada.

The CRA is the federal regulatory agency that administers the Income Tax Act.

The lump-sum value of your earned pension. The commuted value changes based on factors such as age, life expectancy, inflation and interest rates.

An inflation measure computed by Statistics Canada that calculates the change in prices of a fixed set of commodities purchased by Canadians each month. If the combined cost of these goods goes up, inflation increases. The CPI is used to calculate annual cost-of-living increases for pension benefits, also referred to as “indexing”.

A pension plan that defines the ultimate pension benefit to be provided in accordance with a formula, usually based on years of service and earnings. WISE Trust is a defined benefit pension plan.

Learn more on the advantages of a defined benefit pension plan.

Retirement before you reach age 65, in which you may receive a reduced pension or an unreduced pension.

Learn more about this on the retirement page.

An eligible child includes your natural, adopted, or step child in respect of whom you are acting in the role of a parent and who is:

- under age 18; or

- 18 or older but less than 25 and attending full-time, continuous education; or

- 18 or older and suffers from a physical or mental disability that has prevented them from earning a living since reaching 18 or since your death, whichever occurred most recently.

Eligible spouse means, on the relevant date, either of two persons who are

- married to each other; or

- not married to each other but are living together in a conjugal relationship, either:

- continuously for a period of not less than three years; or

- in a relationship of some permanence, if they are the parents of a child, as set out in Section 4 of the Children’s Law Reform Act pursuant to subsection 1 (1) of the Pensions Benefit Act.

On termination of employment, the Plan compares 50 per cent of the commuted value of the member’s deferred pension to the total of their contributions plus interest. If the member’s contributions plus interest equal more than 50 per cent of the commuted value of the pension, then that member is entitled to a refund of the difference, called excess contributions.

An independent regulatory agency, an objective of which is to improve consumer and pension plan beneficiary protections in Ontario.

Learn more about them on FSRA’s website.

The Policy, which is approved by the WSIB and the OCEU as sponsors of the Plan, provides a framework for the financial management of the pension benefits earned under the Plan and the corresponding assets of the trust fund that secure those pension benefits.

A federally legislated act with underlying regulations that outline, among other things, the maximum limits for registered pension plans. The Income Tax Act allows employees and employers to deduct pension contributions from their respective income for tax purposes and sets standards for the benefits a pension plan can provide. It is regulated by CRA.

A method in which pension benefits are adjusted to take into account changes in the cost of living.

A pension plan in which decision making and funding of the benefits is shared jointly by both employees and the participating employer. It’s a pension plan where there is a partnership in the governance of the plan.

The lifetime pension is the amount paid to you for the rest of your life once you retire, inclusive of any further indexation. This amount does not include the bridge benefit, which is paid on top of the lifetime pension up to age 65. Once you reach age 65, the bridge benefit ends and you continue to receive the lifetime pension.

A legislative requirement stipulating that vested entitlements under a pension plan must be used to provide pension payments at retirement and are not available as immediate cash.

A tax-sheltered retirement savings arrangement in which the funds are subject to locking in under pension legislation. Funds in a locked-in retirement savings arrangement cannot be withdrawn prior to the age of 55 and the payment of retirement income from the arrangement must begin no later than the end of the year in which you reach age 71. Examples include annuities, locked-in retirement accounts, life income funds, and other registered pension plans that will accept the commuted value of a deferred pension.

Learn more about this on leaving your employer.

A type of RRSP available to maintain funds that are locked-in as required by pension legislation. These funds must be used to purchase a life annuity or be transferred to a life income fund no later than the end of the year in which you reach age 71.

An employee of a participating employer who is contributing to the Plan or has contributions made on their behalf. Member also includes a former employee of a participating employer who made contributions to the Plan and has either terminated employment or terminated membership in the Plan and (i) retains the right to a deferred pension payable from the Plan or (ii) is receiving a pension payable from the Plan.

This includes the period commencing on the date an employee becomes a member of the Plan until the date the employee terminates the employment that relates to the Plan or terminates membership in the Plan. Any period during which a member was absent from work on a leave of absence, as well as any period of pensionable service transferred into the plan or purchased subject to the Plan’s terms will be included in the calculation of the member’s period of membership. Membership will not be broken for the sole reason that an employee ceased employment with one participating employer and immediately began employment with another participating employer.

An online self-service site for members to log in to view their personal pension details, estimate their pension, request a quote to purchase pensionable service, download forms, tip sheets, the guidebook, and more.

Login to My Pension Resource.

Normal retirement age under the Plan is age 65. The normal retirement age does not compel retirement at age 65, but rather sets the age when unreduced pensions are paid regardless of the years of pensionable service you have under the Plan.

The Workplace Safety and Insurance Board (WSIB), Infrastructure Health and Safety Association (IHSA), Public Services Health and Safety Association (PSHSA), Workplace Safety and Prevention Services (WSPS), Workplace Safety North (WSN), and the Trustees of the Workplace Safety and Insurance Board Pension Plan Fund (WISE Trust).

The deemed value of additional pension benefits purchased for service in previous years. The CRA generally must approve the PSPA before the purchase of additional benefits can be completed and before the purchase can be included in any benefit calculation.

The CRA’s deemed value of the lifetime benefit a member earns during a calendar year under a pension plan, and it affects the member’s RRSP contribution room for the following year.

The pension adjustment is the annual pension amount earned by the member during the year, multiplied by nine, and then the prescribed amount of $600 is subtracted.

The pension adjustment is reported on your T4 tax slip, and your available RRSP contribution room for the following year is reduced by the pension adjustment amount.

Provincial legislation enforced by FSRA, which regulates pension plans in Ontario and determines minimum standards for eligibility, funding, and benefits for Ontario-registered pension plans.

Learn more about the legislation: Pension Benefits Act (PBA).

- the amount of benefits that you are in receipt of under the Workplace Safety & Insurance Act (WSIA) for loss of earnings and any amount supplemented by the WSIB up to the maximum of your regular earnings

- non-bargaining unit lump-sum merit awards

- earnings if you are receiving long-term disability benefits

Pensionable earnings do not include:

- overtime pay

- irregular-hour premiums

- performance bonuses

- job differential pay

- second-language bonuses

- pay in lieu of vacation or Management Compensation Option

- any payment in lieu of a benefit provided by your participating employer

Represents the total years, months and days of service during which you or your employer have contributed to the Plan on your behalf. Subject to the Plan’s terms, it includes any pensionable service you have purchased, transferred in, or service during which you were receiving short-term or long-term disability benefits or while you were in receipt of benefits from a claim filed under the WSIA.

If you are a part-time employee, your pensionable service is calculated as a proportion of the pensionable service that an equivalent full-time employee in the same employment category would accrue. Learn more under pensionable service.

A pension that starts before age 65 and is subject to a reduction for starting your pension early. The reduction for starting your pension early means the pension is reduced by three per cent for each year (and any fraction thereof) your retirement falls before the date you would have qualified for your earliest unreduced pension.

Learn more about this on collecting your pension.

This is a savings arrangement available from most financial institutions that accumulates contributions and investment earnings on a tax-sheltered basis.

The annual statement of earnings and deductions provided to employees and to the CRA by the employer.

The annual statement of pension earnings and deductions provided to retirees and to the CRA by WISE Trust.

An unreduced pension is a pension that is not subject to an age reduction. You may receive an unreduced or lesser reduced pension at age 65 or, earlier provided you have qualified under the early retirement provisions of the factor 85 or 60/20 rule.

Learn more about this on collecting your pension.

A term used in the CPP that refers to the earnings on which CPP and Quebec Pension Plan contributions and benefits are calculated. The YMPE is re-calculated each year according to a formula based on average wage levels. The YMPE is published annually by the CRA.

Canada Pension Plan

A contributory, earnings-related social insurance program that is paid by the federal government. It provides a measure of income to contributors and their families upon retirement, disability, and death. For further details, contact Service Canada.

WTW case management system within eePoint

WTW secure website used to send/receive reports and other confidential member-related data

For more information, refer to subsection 2.5(d)

WTW Pension Administration System.

For more information, refer to subsection 2.5(a)

Financial Services Regulatory Authority of Ontario

An independent regulatory agency whose role is to ensure pension plans meet the legal standard in the Pension Benefits Act (PBA). Their objective is to improve consumer and pension plan beneficiary protections in Ontario.

Income Tax Act

A federally legislated act with underlying regulations that outline, among other things, the maximum limits for registered pension plans. The Income Tax Act allows employees and employers to deduct pension contributions from their respective income for tax purposes and sets standards for the benefits a pension plan can provide. It is regulated by the Canada Revenue Agency (CRA)

Data files that contain employee/member data required to administer pension benefits that are sent bi-weekly from each participating employer to WTW via:

I1 Data File – transmits Demographic & Employment/HR data on a bi-weekly I1 schedule

I2 Data File – transmits Contribution & Payroll data on a bi-weekly I2 schedule

Refer to section 4. Reporting Data and the I1 & I2 Data Interfaces for more information

Jointly Sponsored Pension Plan

A pension plan in which decision making and funding of the benefits is shared jointly by both employees and the sponsor/participating employer. It’s a pension plan where there is a partnership in the governance of the plan. The Plan is a JSPP

Pension Self-Service Pension Website for active, deferred and retired members

Ontario Compensation Employees Union, CUPE Local 1750

Co-Sponsor of the Plan (with WSIB)

Pension Adjustment

The CRA’s deemed value of the lifetime pension benefit earned by a member during a calendar year which affects the member’s RRSP contribution room for the following year. Refer to subsection 6.3 Annual Pension Adjustment Report (I7) for more information

Pension Benefits Act (Ontario)

Provincial pension legislation enforced by FSRA, which regulates pension plans in Ontario and determines minimum standards for eligibility, funding, and benefits for Ontario-registered pension plans

The base salary/compensation received by an employee for their employment position while a member of the Plan.

Refer to X for specific Pensionable Earnings inclusion and exclusions

Note: Contributions must be deducted from Pensionable Earnings in accordance with the Contribution Rate Schedule. Contribution amounts are provided by Participating Employers to WTW for each member via the I2 Data File

Represents the total years, months and days of service during which the employee, or the employer on behalf of the employee, contributes to the Plan or Supplementary Plan and can include service during which an employee is receiving short-term, or long-term disability benefits, or while in receipt of benefits from a claim filed under the WSIA

Determined by the employment statuses for each employee/member as provided by Participating Employers via the I1 Data File, and contributions deducted as provided via the I2 Data File as required, plus any service purchased or transferred in by the employee/member.

Secure File Transfer Protocol

Transmission method by which I1 and I2 Data Files are sent from Participating Employers to WTW

Safe Workplace Associations

Infrastructure Health & Safety Association (IHSA)

Public Services Health & Safety Association (PSHSA)

Workplace Safety & Prevention Services (WSPS)

Workplace Safety North (WSN)

WSIB Employees’ Supplementary Pension Plan (ESPP)

A “top-up” retirement compensation arrangement that provides employees of the WSIB and SWA a pension benefit in excess of the maximum pension benefit permitted under the Plan and the ITA; the Plan and the Supplementary Plan (the “plans”) operate together to provide the same retirement benefit that the employee would have received if the ITA limits did not exist

Sponsored and administered solely by WSIB

Refer to subsection 2.2 The Supplementary Plan for more information

WSIB Employees’ Pension Plan (EPP)

A contributory defined-benefit pension plan registered and regulated under the Ontario Pension Benefits Act (“PBA”) and the federal Income Tax Act (“ITA”)

Jointly sponsored by the WSIB and OCEU and administered by WISE Trust

Refer to subsection 2.1 The Plan for more information

Workplace Safety & Insurance Board

Co-Sponsor (with OCEU) and Participating Employer of the Plan

Sponsor and administrator of the Supplementary Plan

Workplace Insurance and Safety Employee Trust

The Trustees of the Workplace Safety and Insurance Board Employees’ Pension Plan (Board of Trustees)

Legal Administrator of the Plan

Willis Towers Watson

Pension Administration Service Provider for the Plan and the Supplementary Plan

Refer to subsection 2.3 Pension Administration Service Provider for the Pension Plans for more information

Already retired

If you’re already retired

Pension pay dates

Pension payments are made on the first day of each month. However, if your banking institution does not process payments on weekends or statutory holidays, your monthly pension payment will be deposited on the first business day of each month. Contact your banking institution to confirm the timing of direct deposits on non-business days.

What's on this page

- If you're already retired

Information about your pension payments

Your pension payments start on the first of the month following your retirement, provided all the necessary forms and documents are accurately completed and promptly submitted one month prior to your retirement date.

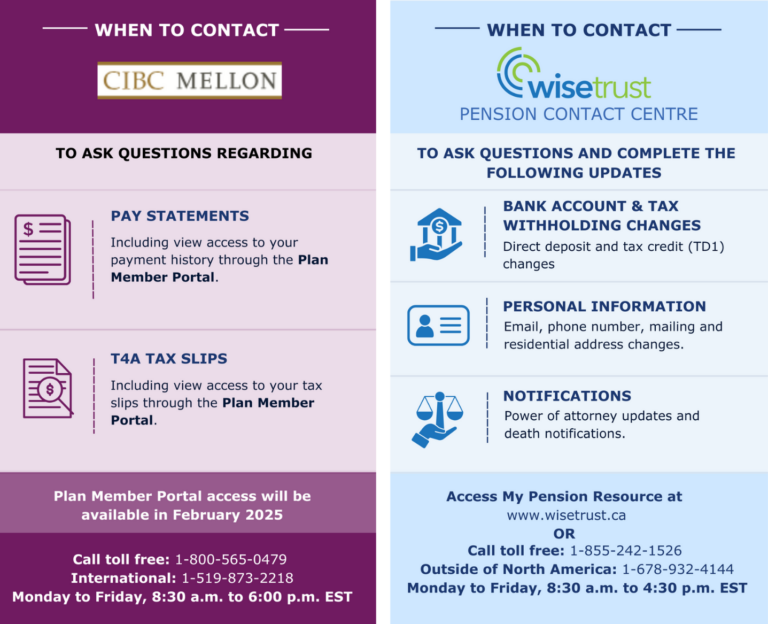

You can access your pay statements and T4A tax slips for periods prior to September 2023 through Workforce Now.

For more recent pay statements and T4A tax slips issued for periods after September 2023, please call CIBC Mellon or log into the CIBC Mellon Plan Member Portal.

Updating your personal and banking information

If you have moved, updated your email, or changed your phone number, make sure you update your personal information through My Pension Resource or by calling the WISE Trust Pension Contact Centre.

If you’re opening a new bank account, let us know as soon as possible. Don’t close your old account until you see your pension has been deposited into your new account.

You can update your banking information by contacting us at the WISE Trust Pension Contact Centre or through My Pension Resource under “Profile.”

Here’s a breakdown of who to contact and where to access the information you need:

What about taxes?

By law, we must deduct taxes from your pension payment, just like your employer did when you were working. Deductions are based on basic federal and provincial income tax guidelines and the personal tax information you reported to us when you retired. We can vary the amount of tax deducted from your WISE Trust pension, if:

- You have additional tax credits, such as a spousal credit, age credit, or tuition credit

- You request that more tax be deducted

To make changes, complete Canada Revenue’s Personal Tax Credit forms and submit them to the WISE Trust Pension Contact Centre.

You can access your pay statements and T4A tax slips for periods prior to September 2023 through Workforce Now.

For more recent T4As issued for periods after September 2023, please call CIBC Mellon or log into the CIBC Mellon Plan Member Portal.

Returning to work

If you’re rehired by a participating employer as a permanent employee after you begin receiving your pension, your payments will be suspended while you are a permanent employee, up to December 1 of the calendar year in which you reach age 71. When you retire again, your pension will be recalculated.

If you are rehired by a participating employer as a temporary or contract employee after you begin receiving your pension, your pension will not be suspended.

What about other income sources?

Retirement means it’s time to enjoy the lifetime pension you’ve earned. In addition to your WISE Trust pension, you’ll collect a government pension and may also have personal retirement savings, such as a registered retirement savings plan or tax-free savings account. The Federal Government administers the Canada Pension Plan (CPP) and Old Age Security (OAS) retirement programs.

If you have questions related to CPP or OAS, you can learn more about them on the Government of Canada’s website for CPP and OAS.

Designating a Power of Attorney

Granting a power of attorney to someone you trust can help you manage your affairs in the event you are incapacitated. You don’t have to designate a power of attorney, and you can learn more by reviewing the Government of Canada’s resource page regarding powers of attorney. If you appoint a power of attorney, provide the WISE Trust Pension Contact Centre a complete copy of the Power of Attorney, making sure it shows all signatures and dates, and contact information for the Power of Attorney.

When you pass away

If you pass away after your pension has started, your survivor or the executor of your estate should notify the WISE Trust Pension Contact Centre immediately.

Need to update your contact information or report a death?

To help you manage important updates such as a change in mailing address or phone number, reporting a death, or asking about post-retirement benefits, we’ve provided additional contact details for your convenience. To ensure your request is processed smoothly, please reach out to the following:

- The WISE Trust Pension Contact Centre

- Your former employer (details below)

- Your post-retirement benefits carrier if applicable (details below)

| Former Employer | Department/Benefits Carrier | Contact Details | Email/Website |

|---|---|---|---|

| WSPS | WSPS People & Culture Department | 905-614-2113 | hr@wsps.ca |

|

Manulife Policy: 0631400 Plan Number: 043 |

1-800-268-6195 PO BOX 11006, Stn Centre-Ville Montreal, QC H3C 4T8 DEATH CLAIMS: PO BOX 400 Stn Place-D'Armes Montreal, QC H2Y 3H1 |

www.manulife.ca | |

| WSN | WSN HR Dept | 705-474-7233 | Pensions@workplacesafetynorth.ca |

| Manulife |

1-877-481-9169 PO BOX 400 Stn Place-D'Armes Montreal, QC H2Y 3H1 |

www.manulife.ca | |

| IHSA | IHSA HR Department | 1-800-263-5024 | ihsahumanresources@ihsa.ca |

| Manulife | 1-800-268-6195 | www.manulife.ca | |

| WSIB | WSIB HR Benefits Department | 416-344-6007 | TotalRewards@wsib.on.ca |

Manulife

|

1-866-318-2727 | www.manulife.ca | |

| PSHSA | PSHSA HR Dept |

905-410-1852

PO BOX 11006, Stn Centre-Ville Montreal, QC H3C 4T8 |

HRgeneral@pshsa.ca |

|

Manulife Policy: 0631400 |

1-866-318-2727 | www.manulife.ca | |

| WISE Trust Pension Contact Centre | 1-855-242-1526 | ||