On July 1, 2025, your pension contribution rates will increase by 0.6 percent of your pensionable earnings.

Effective July 1, 2025, the percent of pensionable earnings below the YMPE* will increase to 8.8%, and the percent of pensionable earnings above the YMPE will increase to 10.6%.

To learn more about the plan contribution formula and how you contribute to your pension, visit Pension Contributions.

*The Year’s Maximum Pensionable Earnings (YMPE) is set by the Government of Canada, which is $71,300 for 2025.

Why is this happening?

Since July 1, 2020, member contribution rates have gradually increased by 0.6 percent of pensionable earnings per year and will do so until the funding for the Plan reaches a 50/50 employer-member cost-sharing ratio. By doing this together, we help maintain a sustainable pension plan!

Learn more about how your WISE Trust pension is funded.

When will this be reflected on my pay?

Your contributions are deducted directly from your bi-weekly pay. Depending on which participating employer you work for, you’ll see the contribution increase on the following pay date:

| WISE Trust Participating Employer | Pay Date* |

|---|---|

| Workplace Safety and Insurance Board (WSIB) | July 24, 2025 |

| Infrastructure Health and Safety Association (IHSA) | July 24, 2025 |

| Public Services Health and Safety Association (PSHSA) | July 24, 2025 |

| Workplace Safety and Prevention Services (WSPS) | July 24, 2025 |

| Workplace Safety North (WSN) | July 24, 2025 |

| Workplace Insurance and Safety Employee Trust (WISE Trust) | August 7, 2025 |

*Contribution rate changes take effect on the first day of the pay period either on or immediately following the July 1st contribution rate effective date.

Please be advised that there may be a labour disruption at Canada Post in the coming days. In the event of a postal service disruption, you may experience delays in mail delivery. My Pension Resource is the most efficient way for members to send and receive important information about their pension.

To minimize the impact of a strike, we encourage you to upload your pension-related documents via My Pension Resource using the Messages feature. Make sure to also set your Communication Preferences to electronic delivery under the Profile page so that you can always access your important documents online.

Not registered on My Pension Resource?

To ensure you always receive updates and information about your pension, sign up today for your My Pension Resource account in a few quick steps:

- You will need your Employee/Pension ID number, last name, personal email address and date of birth to get started

- Select “Create User” and follow the instructions to create your username, password, and security questions.

If you have any questions or require assistance, please contact our WISE Trust Pension Contact Centre.

Cheque payments

If you still receive your monthly pension payment by cheque, we strongly encourage you to enroll in direct deposit so you won’t be affected by postal disruptions or delays. Please contact the WISE Trust Pension Contact Centre or visit My Pension Resource to provide your banking information and update your payment method.

All non-critical correspondence will be securely stored until normal postal service resumes.

We will continue to closely monitor this situation and provide updates on our website.

For more information about the Canada Post Labour strike, please visit canadapost.ca.

[Toronto, ON — February 27, 2025] — WISE Trust, the leading pension administrator of retirement solutions for Workplace Safety and Insurance Board Employees in Ontario, is pleased to announce a robust net return of 11.3% for the fiscal year 2024. This strong investment performance increases assets of the WSIB Employees’ Pension Plan (Plan) to a total of $4.46 billion, enhancing long-term sustainability of the Plan and its ability to deliver financial security to members in retirement.

In a year marked by economic challenges and market volatility, WISE Trust remained committed to delivering solid financial outcomes for members by applying prudent risk management and disciplined investment strategies which produced exceptional returns. This acceleration in performance highlights the value of the Plan’s collaborative partnership with its exclusive investment manager, Investment Management Corporation of Ontario (IMCO), in providing the Plan with diversification of investments across asset classes, contributing to the boost in annual net return.

Christopher Brown, Chief Executive Officer of WISE Trust says, “The return for 2024 was led by strong results in our Canadian, global and emerging market public equities, and global credit portfolios. The WISE Trust Board of Trustees and management team remain diligently focused on balancing risk and reward to deliver strong and sustainable outcomes for members. These results in implementing the Plan’s asset strategy further demonstrate the value of WISE Trust’s collaborative partnership with IMCO.”

“We are very pleased to have achieved this solid 11.3% net return on WISE Trust’s investment portfolio for 2024,” said Mr. Brown.

He added, “Despite a challenging economic environment, this impressive return aids in enhancing benefit security for our 10,000+ members and beneficiaries. We have again this year comfortably exceeded the target return for the portfolio, which will serve the Plan well as we navigate the uncertainty that has characterized the early months of 2025.”

About WISE Trust

The Workplace Safety and Insurance Board Employees’ Pension Plan (the Plan) is a jointly sponsored defined benefit pension plan co-sponsored by the Workplace Safety and Insurance Board (Ontario) and the Ontario Compensation Employees Union, CUPE Local 1750 (OCEU). The WISE Trust Board of Trustees (made up of individual trustees appointed by the WSIB and OCEU) is the legal administrator of the Plan.

On July 1, 2020, the Plan became the first pension plan in Ontario to convert from a single employer pension plan to a jointly sponsored pension plan.

IMCO is the exclusive investment manager for the Plan, operating to implement the investment policy and strategic asset allocation set by the WISE Trust Board of Trustees.

For media inquiries, please contact:

Monique Patrick

WISE Trust, Communications Specialist

communications@wisetrust.ca

Attention Members of the Workplace Safety & Insurance Board Employees’ Pension Plan

Thursday, February 20th is Pension Awareness day in Ontario.

This day is the perfect opportunity to reflect on your retirement planning, stay informed, and take the necessary steps to achieve a more secure financial future for you and your family.

Pension Awareness Day highlights the importance of pension savings and the benefits of workplace pension plans, such as the plan offered by WISE Trust. Contributing to a pension plan, especially a defined benefit plan, plays a crucial role in your financial future, helping ensure a stable and predictable income during retirement.

Benefits of Contributing to a Pension Plan

Here are some key benefits of contributing to any pension plan, including the WISE Trust plan:

- Financial Security in Retirement: Contributing to a pension plan can provide significant financial security and peace of mind for your retirement.

- Tax Advantages: Contributions to pension plans are tax-deductible, and the growth of investments within the plan is tax-deferred until withdrawal.

- Employer Contributions: Many pension plans include employer contributions, which can significantly boost your retirement savings.

- Ease of Contribution: Contributions are made through payroll deductions, making it easy and consistent to save for retirement.

- Portability: Most pension plans allow you to transfer your savings if you change jobs, ensuring your retirement savings continue to grow.

The Advantages of your WISE Trust Pension Plan

WISE Trust offers a defined benefit pension plan, which provides numerous advantages for your retirement security. Here are some key benefits:

- Predictable Retirement Income: A defined benefit pension plan guarantees a specific monthly benefit upon retirement, based on a formula that considers your salary and years of service. This predictability allows you to plan your retirement with confidence, knowing precisely what your income will be. Once you start receiving a pension, you will continue to do so for the rest of your life.

- Protection Against Market Fluctuations: Unlike defined contribution plans, where your retirement income depends on investment performance, a defined benefit plan shields you from market volatility. Your benefits are secure and not subject to the ups and downs of the financial markets.

- Ancillary Benefits: Additional benefits provided by WISE Trust include inflation protection, early retirement benefits, and survivor benefits. With other retirement savings plans like defined contribution pension plans or individual or group RRSPs, individuals may be able to buy a lifetime annuity that includes some additional benefits such as inflation protection. However, these extra features often come at a high cost, which can reduce the overall amount available for generating a pension income stream.

Pay your pension some attention

To learn more about your WISE Trust pension, visit Pension 101 or visit Financial Services Regulatory Authority of Ontario for general pension information and resources.

In early February 2025, WISE Trust pensioners will receive a letter by mail from CIBC Mellon, our pension payment service provider, announcing the launch of the new Pensioner Information Network – Plan Member Portal, a secure self-service website that offers convenient, anytime access to monthly pension payment details and tax slips.

The CIBC Mellon self-registration letter will provide instructions on how pensioners can register for and access the Plan Member Portal.

Plan Member Portal Features

- View pension payment details

- View and print monthly pension payment history

- View and download and print T4A tax slips

- View profile information (address, banking information, income tax withholding details including extra tax and personal exemption amounts)

Who to Contact?

The Plan Member Portal self-registration letters will be mailed to all pensioners in early February. For assistance with the registration process, contact CIBC Mellon. They are also available to help answer questions regarding the Plan Member Portal, pay statements or T4A tax slips.

The WISE Trust Pension Contact Centre will remain available to support members with all other pension-related inquiries, including updating email, phone number, mailing and residential addresses, direct deposit and tax credit (TD1) information.

For a complete list of who to contact and where, click here and review the section entitled Updating your personal banking information.

Voluntary Registration

The transition to digital self-service is a part of our ongoing commitment to enhance the quality and reliability of our services for our valued members.

Registering to access the Plan Member Portal is optional. Pensioners who choose not to register will continue to receive pay statements and tax slips via mail as usual.

Retired and deferred members benefit from inflation protection

To help our retired and deferred members’ pensions keep up with inflation, lifetime pensions will increase by 2.0% in accordance with the Plan’s indexation provisions. The increase is effective January 1, 2025, and equals 75% of the percentage change in the Consumer Price Index (CPI). This increase applies only to lifetime pensions – bridge benefits received before age 65 are not indexed.

Retired members will see their monthly pension payments increase as of the effective date. Those with pension payments that started part way through 2024 will receive a prorated indexation increase. For example, a member with pension payments that began on July 1, 2024, will receive half of the annual indexation increase.

Learn more about indexation.

Canada Post workers are currently on strike, and here’s what you need to know

We are working to ensure you have the pension information you need in the event of a prolonged disruption.

To minimize the impact of the strike, we encourage you to upload your pension related documents via My Pension Resource using the Secure Message feature. Make sure to also set your Communication Preferences to email so that you can always access your important documents online.

Not registered on My Pension Resource?

Simply select the Register here option and follow the instructions listed. If you have any questions or require assistance, please contact our WISE Trust Pension Contact Centre.

Cheque payments

If you receive your monthly pension payment by cheque, we encourage you to enroll by direct deposit, so you won’t be affected by postal disruptions or delays. Please contact the WISE Trust Pension Contact Centre or visit My Pension Resource to provide your banking information and update your payment method.

All non-critical correspondence will be securely stored until normal postal service resumes.

We will continue to closely monitor this situation and provide updates on our website.

For more information about the Canada Post Labour strike, please visit canadapost.ca.

There have been many media reports about the CrowdStrike – Microsoft outage that impacted airlines, banks, and many other organizations globally Friday.

The outage was caused by a defect in an update from the cybersecurity provider CrowdStrike, which caused cascading failures on computers using its cybersecurity application with Microsoft Windows. WISE Trust does not use CrowdStrike and there is NO IMPACT to WISE Trust systems. Our team was aware of the issue and worked with our IT provider and major vendors to monitor the situation. Some of our vendors experienced minor issues, and these issues were quickly addressed through their own cybersecurity response protocols. As a result, there is NO IMPACT to pension payments or plan members’ ability to interact with the Plan.

We will continue to monitor the situation and post updates if there are any significant developments.

On July 1, 2024, your pension contribution rates will increase by 0.6 per cent of your pensionable earnings.

Effective July 1, 2024, contribution rate (A), the per cent of pensionable earnings below the YMPE*, will increase to 8.2% and contribution rate (B), the per cent of pensionable earnings above YMPE, will increase to 10.0%.

Learn more about how you contribute to your pension.

*Year’s maximum pensionable earnings (YMPE) is set by the Government of Canada, which is $68,500 for 2024.

Why is this happening?

Since July 1, 2020, member contribution rates have gradually increased by 0.6 per cent of pensionable earnings per year and will do so until the funding for the Plan reaches a 50/50 employer-member cost-sharing ratio. By doing this together, we help maintain a sustainable pension plan!

When will this be reflected on my pay?

Your contributions are deducted directly from your bi-weekly pay. Depending on which participating employer you work for, you’ll see the contribution increase on the following pay date:

| WISE Trust Participating Employer | Pay Date* |

|---|---|

| Workplace Safety and Insurance Board (WSIB) | July 25, 2024 |

| Infrastructure Health and Safety Association (IHSA) | July 25, 2024 |

| Public Services Health and Safety Association (PSHSA) | July 25, 2024 |

| Workplace Safety and Prevention Services (WSPS) | July 25, 2024 |

| Workplace Safety North (WSN) | July 25, 2024 |

| Workplace Insurance and Safety Employee Trust (WISE Trust) | August 8, 2024 |

*Contribution rate changes take effect on the first day of the pay period either on or immediately following the July 1st contribution rate effective date.

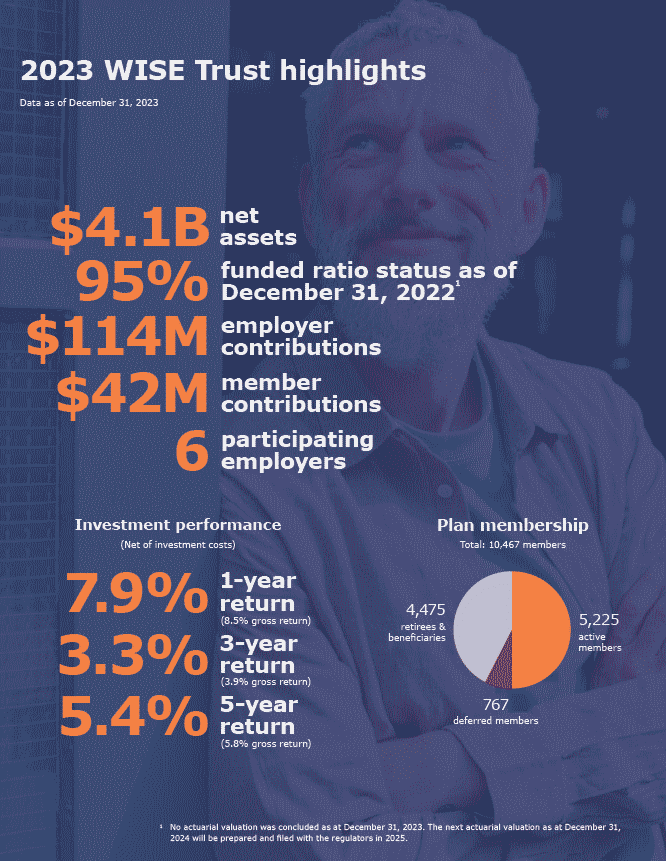

Our 2023 Annual Highlights for Members marks WISE Trust’s fourth annual report. With three full calendar years under our belt since converting to a Jointly Sponsored Pension Plan (JSPP), we are proud to see our membership grow to over 10,000 active, retired, and deferred members.

Our 2023 edition provides an outlook on a progressive year dedicated to collaboration, growth and continued delivery of our defined benefit pension promise to members. This report provides a year in review and explores our investment performance, membership highlights and much more.

Key Highlights from 2023

What is included in the Highlights for Members report?

- Letter from the Co-Chairs of the Board of Trustees

- Letter from our CEO, Christopher Brown

- Data on our financial performance and funded status

- Member survey results

- Investment insights and more!